How to Compare Installment Loan Offers

Written by: Jacob S.

Published on:

Loan terms can vary dramatically from one lender to the next, even for the same borrower profile. Two lenders might approve the same applicant for the same amount yet quote wildly different costs. That gap can translate to hundreds or even thousands of dollars over the life of the loan.

Knowing how to compare offers correctly is one of the most valuable skills in personal finance. This guide walks through a clear, practical checklist based on standard lending disclosures and Truth in Lending Act (TILA) concepts, so every comparison is apples-to-apples.

Key Takeaways

- APR is the only reliable number for comparing loan costs because it folds in both the interest rate and lender fees into a single figure, making offers with different fee structures directly comparable.

- A lower monthly payment rarely means a cheaper loan. A longer term stretches payments out, and interest accumulates over every additional month, often adding hundreds of dollars to the total repayment cost.

- Fees are where loan costs hide. Origination fees, NSF fees, and prepayment penalties do not always appear in the headline offer summary, and the only way to catch them is to read the full loan agreement before signing.

- Lender credibility is part of the comparison. A competitive rate from an unverified lender with no clear disclosures, no physical address, or guaranteed approval claims is a warning sign, not a deal.

If you are new to installment loans, it helps to understand how they work before comparing offers. The steps below assume you already have two or more loan offers in hand and are ready to evaluate them side by side.

Installment Loan Comparison Checklist

Before diving into the step-by-step process, here is a high-level overview of the seven factors that matter most when comparing loan offers.

| Factor | What to Look For | Why It Matters |

|---|---|---|

| APR | Lowest overall rate | Reflects the true cost of borrowing |

| Monthly Payment | Comfortably affordable | Determines day-to-day budget impact |

| Loan Term | Shorter vs. longer | Affects total interest paid |

| Fees | Origination, late, NSF | Uncovers hidden costs |

| Total Repayment | Total dollars out of pocket | Reveals the real price of the loan |

| Flexibility | Prepayment, hardship options | Protects if circumstances change |

| Lender Trust | Reviews, disclosures, credentials | Guards against predatory practices |

Step-by-Step: How to Compare Loan Offers Side by Side

Here are the steps to get an accurate comparison between installment loan offers:

Step 1: Gather All Loan Offers in One Place

Start by collecting every offer into a single view, whether that is a notepad, a spreadsheet, or a printed table. For each offer, record:

- Loan amount

- Annual Percentage Rate (APR)

- Monthly payment

- Loan term (number of months)

- All fees

Having everything in one place eliminates the risk of misremembering details and makes direct comparison straightforward.

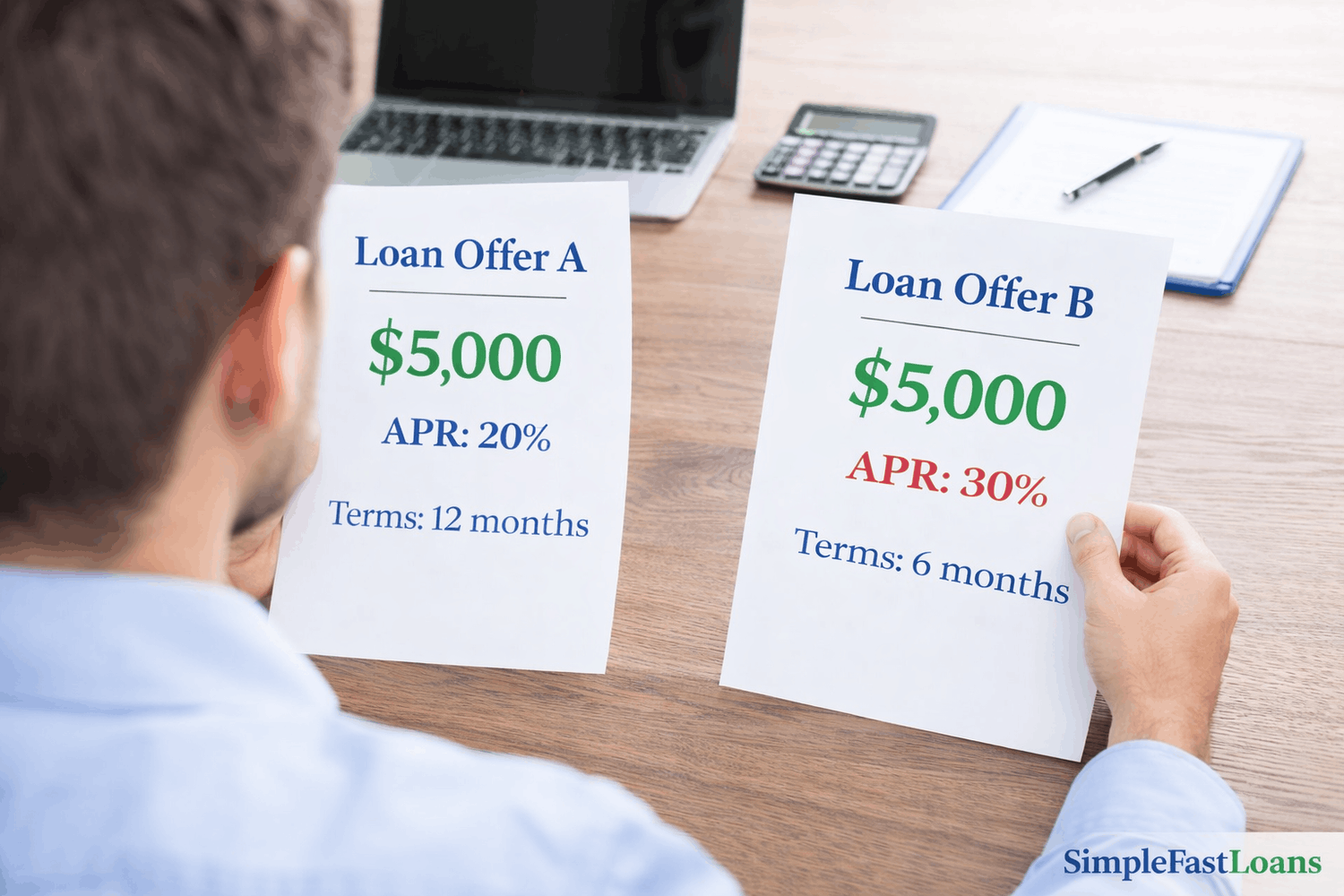

Step 2: Compare APR, Not Just the Interest Rate

APR is the single most important number to compare across loan offers. It combines the interest rate with any lender fees, expressing the total annual cost as one percentage. That is why the Truth in Lending Act requires lenders to disclose it prominently.

The interest rate alone can be misleading:

- Loan A: 15% interest rate, 18% APR

- Loan B: 17% interest rate, 17% APR

Loan B has a higher stated interest rate but a lower APR, making it the less expensive option once fees are factored in. Always lead with APR when ranking offers.

Step 3: Check How Lenders Pull Your Credit

When shopping multiple lenders, pay attention to whether each one uses a soft credit check or a hard credit check to generate their offer:

- Soft inquiry: Shows you estimated terms without affecting your credit score, making it safe to check multiple lenders before committing.

- Hard inquiry: Recorded on your credit report and can cause a small, temporary dip in your score.

For borrowers with fair or bad credit who are cautious about protecting their score, confirming the inquiry type before applying is a smart first step.

Step 4: Calculate the Total Cost of the Loan

Monthly payment amounts are useful for budgeting, but they do not tell the whole story. The total repayment cost is the amount that actually leaves a borrower's bank account over the life of the loan.

Formula: Total Paid = Monthly Payment x Number of Payments

Here is a common comparison trap:

| Scenario | Monthly Payment | Term | Total Paid |

|---|---|---|---|

| Option A | $300 | 24 months | $7,200 |

| Option B | $200 | 48 months | $9,600 |

Option B looks more manageable every month, but it costs $2,400 more overall. A lower monthly payment almost always means a higher total cost when the term is longer.

Step 5: Evaluate Loan Term Length

Loan term is a lever that directly trades monthly affordability against total interest paid.

Shorter terms:

- Higher monthly payments

- Less total interest paid

- Faster path to being debt-free

Longer terms:

- Lower monthly payments

- More total interest paid over time

- Greater flexibility in monthly cash flow

The right choice depends on the borrower's situation. Someone with a tight monthly cash flow may need the lower payment, even knowing it costs more in the long run. Someone with room in the budget should lean toward the shorter term to minimize total cost.

Step 6: Identify All Fees

Fees are where loan costs quietly accumulate. The key fees to review in every loan agreement include:

- Origination fee: Charged upfront for processing the loan, typically ranging from 1% to 10% of the loan amount. A $5,000 loan with a 5% origination fee starts with a $250 cost before making a single payment.

- Late payment fees: Triggered when a payment is missed or late. These vary widely by lender.

- NSF or returned payment fees: Charged when a payment fails due to insufficient funds.

- Prepayment penalties: Rare but critical to check. Some lenders charge a fee for paying off a loan early, which eliminates the benefit of accelerated payoff.

Reading the full loan agreement, not just the summary page, is the only reliable way to catch all fees before signing.

Step 7: Review Monthly Payment Affordability

General budgeting guidance suggests keeping total debt payments (excluding a mortgage) below 15% to 20% of monthly take-home pay to avoid pushing your debt-to-income (DTI) ratio too high.

Two situations to watch for:

- Over-borrowing: Taking a larger loan than needed because it was offered, leading to a higher payment than necessary.

- Payment stacking: Carrying multiple loan payments simultaneously, which can strain a budget even when each payment seems manageable.

If the monthly payment for a loan offer requires cutting essential expenses or leaves no cushion for unexpected costs, the loan terms may not be the right fit, regardless of the APR.

Step 8: Check Flexibility and Borrower Protections

This step is frequently overlooked, but it matters most when life does not go as planned. Before signing, confirm whether the lender offers:

- Early payoff without penalty: The ability to pay off the loan ahead of schedule and save on interest.

- Hardship programs: Temporary payment deferral or modification options if income is disrupted.

- Payment date changes: The ability to shift the due date to align with a paycheck schedule.

Lenders that offer these options provide meaningful protection. Lenders that do not may leave borrowers without recourse during a difficult period.

Step 9: Verify Lender Credibility

Not every lender operates with equal transparency or integrity. Before moving forward with any offer, research the lender directly.

Signals of a trustworthy lender:

- Verified rating with the Better Business Bureau (BBB)

- Consistent positive reviews across multiple platforms

- Clear, written disclosures before any application

- A physical address and verifiable contact information

- Licensing in the borrower's state

Red flags to walk away from:

- Guaranteed approval claims (legitimate lenders always evaluate creditworthiness)

- Pressure to apply immediately before reviewing terms

- No verifiable state licensing

- Unclear or missing fee disclosures

- Requests for upfront payment before receiving funds

Side-by-Side Example: Comparing Two Real Loan Offers

Here is a practical illustration of how these steps play out.

| Feature | Loan A | Loan B |

|---|---|---|

| Loan Amount | $1,000 | $1,000 |

| APR | 18% | 24% |

| Monthly Payment | $92 | $78 |

| Term | 12 months | 18 months |

| Total Cost | $1,104 | $1,404 |

Loan B appears more attractive every month, with a $14 lower payment. But over the full term, it costs $300 more in total repayment. That difference is the price of a lower monthly obligation, and it is easy to miss without doing the math.

Real-World Scenarios: How Loan Comparisons Play Out

Understanding loan math is useful, but seeing how it applies in real situations makes the decision clearer. Here are a few realistic scenarios borrowers commonly face:

| Scenario | Situation | Key Numbers | What It Looks Like | Takeaway |

|---|---|---|---|---|

| Emergency Expense (Low Cash Flow) | Needs $2,000 for car repair | Loan A: $185 × 12 = $2,220 Loan B: $110 × 24 = $2,640 | Lower payment feels safer, but costs ~$400 more overall | Lower monthly payments often increase the total cost significantly |

| Hidden Fee Trap | Comparing $3,000 loans | Loan A: 16% APR, no fee Loan B: 13% rate + 8% fee ($240) | Loan B looks cheaper until fees are included | Always use APR — fees can reverse which loan is cheaper |

| Over-Borrowing | Approved for $3,500, but only needs $1,500 | Larger loan = higher payment + more interest | Accepting full approval increases the cost unnecessarily | Borrow only what you actually need |

| Flexibility vs Cost | Slightly higher APR loan with protections | Includes hardship options + no prepayment penalty | Costs slightly more but reduces risk during income disruption | Flexibility can outweigh a slightly lower APR |

Common Mistakes to Avoid When Comparing Loans

Even careful borrowers fall into predictable traps. The most common ones to avoid:

- Focusing only on the monthly payment without calculating the total repayment cost

- Ignoring fees, especially origination fees, which affect the effective loan amount

- Skipping the total cost calculation entirely

- Automatically choosing the longest available term to get the lowest payment

- Not verifying the lender's legitimacy before submitting an application

When an Installment Loan May Not Be the Right Option

Responsible borrowing starts with honestly evaluating whether a loan is the best path forward. Before applying, consider whether any of these alternatives fit the situation:

- Payment plans with providers: Many medical offices, utilities, and service providers offer structured payment arrangements without interest.

- Local and federal assistance programs: Emergency assistance funds exist for housing, utilities, food, and medical costs.

- Credit union loans: Credit unions frequently offer lower rates than traditional lenders, particularly for members.

- Family or community resources: Informal borrowing arrangements, when structured clearly, can avoid interest entirely.

If there is genuine uncertainty about the ability to repay a loan on schedule, taking on that debt may compound financial stress rather than relieve it. Exploring non-debt options first is always worth the effort.

Red Flags to Watch For

| Red Flag | What It Means | Why It Matters |

|---|---|---|

| Guaranteed approval | No real underwriting process | Legitimate lenders always assess the ability to repay |

| Missing APR | Only shows payment or interest rate | Hides the true cost of the loan |

| Pressure to act fast | “Limited-time” or urgent offers | Discourages proper comparison |

| Upfront fees | Asked to pay before receiving funds | A common sign of scams |

| No business transparency | No address, license, or reviews | Hard to verify legitimacy |

Related: Common loan scams to avoid

Tools for Comparing Loan Offers

Several tools make the comparison process easier:

- Loan comparison calculators: Available through many financial websites, these allow side-by-side APR and total cost comparisons with minimal manual math.

- Spreadsheets: A simple table in Google Sheets or Excel works well for tracking multiple offers at once.

- Budgeting apps: Tools like YNAB or Mint help assess whether a monthly payment fits within an existing budget before committing.

Final Checklist: Before Signing Any Loan

Use this checklist as the final gate before accepting any installment loan offer.

- Compared the APR across all offers, not just the interest rate

- Calculated the total repayment cost for each offer

- Reviewed all fees, including origination and prepayment penalties

- Confirmed the monthly payment is genuinely affordable

- Understood the trade-off between term length and total cost

- Verified the lender's legitimacy through reviews and disclosures

- Explored non-loan alternatives first

The Bottom Line

The best installment loan is not the one with the lowest monthly payment or the highest approved amount. It is the one with the lowest total cost that fits comfortably within a real budget and comes from a lender that operates transparently.

Rushing through a loan comparison to reach a decision faster almost always costs more in the long run. Taking the time to work through each step in this checklist puts every borrower in the strongest possible position before signing.

When you’re ready, you can apply online with Simple Fast Loans in just a few minutes to check your options and see potential offers.

Related Frequently Asked Questions (FAQs)

Here are questions people often ask about comparing installment loans:

What is the difference between APR and interest rate?

The interest rate reflects only the cost of borrowing the principal. APR includes the interest rate plus any lender fees, making it the more accurate measure of a loan's true annual cost.

How do you know which loan is actually cheaper?

Calculate the total repayment for each offer: monthly payment multiplied by the number of payments. The offer with the lower total repayment is cheaper overall, even if its monthly payment is higher.

Does a longer loan term always cost more?

In nearly every case, yes. A longer term means more payment periods, and interest accrues over each one. The only exception would be a loan with a dramatically lower APR that offsets the extended timeline, which is uncommon.