What Are Direct Deposit Loans?

Written by: Jacob S.

Published on:

Updated on:

When life throws unexpected expenses your way—a surprise medical bill, urgent car repair, or looming rent payment—waiting weeks for loan approval isn't an option. Direct deposit loans have emerged as a popular solution for these financial emergencies, promising cash in your account within hours or days rather than weeks.

However, before diving into this fast-funding world, it's essential to understand what these loans truly offer, their associated costs, and whether they're the right choice for your specific situation.

Key Takeaways

- Direct deposit loans provide quick cash, but actual funding times depend on your bank, lender policies, and how complete your application is.

- Different loan types—installment, credit lines, title loans, and cash advances—offer varied pros and cons, so choose based on your financial situation and risk tolerance.

- Online applications and upfront terms make borrowing easier, but always read the fine print to avoid hidden fees or confusing conditions.

- Stable income, a bank account in good standing, and prepared documents boost your approval chances, even with less-than-perfect credit.

- Use direct deposit loans for true emergencies only, and always have a clear repayment plan to avoid long-term debt traps.

What Are Direct Deposit Loans?

Direct deposit loans are short-term or installment-based personal loans in which funds are deposited directly into your bank account once approved. They’re typically used for emergency expenses like medical bills, car repairs, or rent. These loans are usually unsecured, meaning you don’t need to offer collateral, although secured options exist.

Think of direct deposit loans as the express lane of personal lending. Once approved, funds land directly in your bank account—no waiting for checks in the mail or trips to pick up cash. These loans typically fall into the short-term or installment category and rarely require collateral, making them accessible to borrowers who don't own valuable assets.

The appeal is obvious: speed and convenience. The reality? These benefits often come with trade-offs worth understanding upfront.

Related: Stop guessing when pending deposits will clear

Your Direct Deposit Loan Options

- Installment Loans provide a lump sum upfront with fixed monthly payments over several months to years. This structure works well for borrowers who value predictable budgeting and prefer knowing exactly when their debt will be paid off.

- Lines of Credit offer maximum flexibility, where lenders approve a maximum amount that can be drawn from as needed. Interest only applies to the amount used, and once repaid, the credit becomes available again.

- Title Loans use vehicle titles as collateral, enabling quick approval even with poor credit. However, defaulting means losing transportation, which can create even bigger financial problems.

- Credit Card Cash Advances allow existing cardholders to access cash instantly through ATMs or bank withdrawals. While convenient for emergencies, they typically carry higher interest rates and fees than regular purchases.

The Pros and Cons of Direct Deposit Loans

| Pros | Cons |

|---|---|

| Fast access to emergency funds | “Same-day funding” depends on your bank and when the loan is approved |

| Simple, online application process | Some lenders may still deny applicants with recent bankruptcies or unpaid loans |

| Available to borrowers with bad credit | Short terms may result in higher monthly payments |

| Funds are deposited directly into your account | |

| No collateral required (for unsecured) |

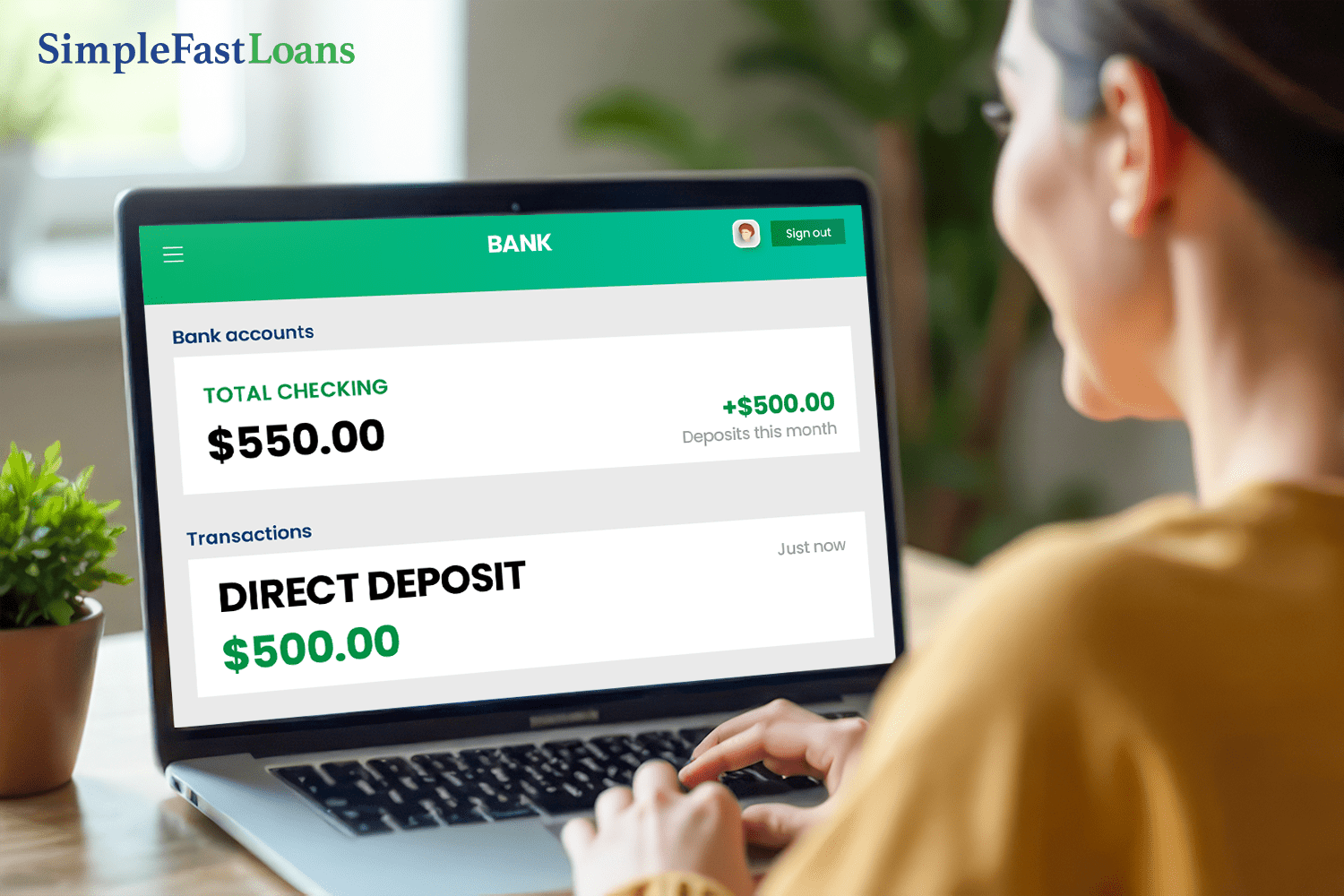

Get a Direct Deposit Loan from Simple Fast Loans

Many lenders offer direct deposit loans to borrowers with less-than-perfect credit. These loans are often more flexible than traditional bank loans and may focus more on income and banking history than on your credit score alone.

At Simple Fast Loans, we conduct a soft credit check as part of the application process to better understand your eligibility. This won’t impact your credit score. If approved, funds are deposited directly into your account, often within one business day**.

The Benefits of a Direct Deposit Loan and What They Mean

Direct deposit loans offer lightning-fast access to funds. Many lenders can deposit money within 24 to 48 hours of approval, with some fintech companies even offering same-day funding. This speed can be genuinely valuable during true emergencies, though processing times still depend on your bank and application completeness. Here are some additional benefits to consider:

| Benefit | What It Means | Reality Check |

|---|---|---|

| Lightning-Fast Access | Many lenders deposit funds within 24 hours of approval; some offer same-day funding via real-time payment systems. This is especially helpful in emergencies. | “Fast” doesn’t always mean “instant.” Delays can happen due to bank processing times, incomplete applications, or late submissions. |

| Streamlined Online Process | The entire loan experience happens online. No in-person visits or paperwork hassle. | Online-only services offer less personal interaction, which may leave some borrowers with unanswered questions. |

| Transparent Terms (When Done Right) | Good lenders show interest rates, fees, and repayment details upfront, helping borrowers make smart choices. | Some lenders still hide fees in fine print or use confusing language—so always read the full loan agreement. |

Maximizing Your Approval Chances

Income stability matters most to lenders. They want to see consistent earnings, even from gig work or freelancing. An active checking account in good standing is non-negotiable, and having all documentation ready speeds up the process significantly.

While many lenders accept borrowers with poor credit, better scores still unlock lower rates and better terms. If time allows, consider quick credit improvements before applying.

Related: 26 Gig Jobs that Pay Weekly

Income Stability Matters Most

Lenders want to see consistent income, even if it's not traditional employment. Gig workers, freelancers, and contractors can often qualify by providing bank statements or tax documents showing regular earnings.

Banking Relationship Requirements

An active checking account is non-negotiable for direct deposit loans. The account should be in good standing with no recent overdraft fees or bank fees, as these can signal financial instability to lenders.

Documentation Readiness

Have identification, proof of income, and bank account information readily available. Complete applications with all required documents typically process faster than those that are missing information.

Credit Score Considerations

While many direct deposit lenders accept borrowers with less-than-perfect credit, better scores still unlock lower rates and better terms. If time allows, consider quick credit improvements like paying down existing balances or disputing errors.

Missing documents? Getting personal loans without proof of income

Debit Card Loans: Instant Funding Straight to Your Card

For borrowers who need money even faster than next-business-day deposits, some lenders offer debit card loans. Instead of sending funds to your bank account through standard ACH transfers, lenders can push the money directly onto your active debit card.

This method uses real-time payment networks, which means you could access your funds within minutes of approval, not hours or days. Debit card loans are especially helpful when:

- You don’t want to wait for traditional bank deposit processing times.

- You’re facing a true emergency like overdue rent, utilities, or urgent travel.

- You prefer funds loaded onto a card you can immediately swipe or withdraw at an ATM.

Keep in mind that availability depends on your lender and whether your bank participates in instant debit card transfers. While the convenience is unmatched, fees or slightly higher interest rates may apply for this faster option.

Secured vs. Unsecured Options

Here is a comparison between secured and unsecured direct deposit loans:

Secured Loans: Lower Rates, Higher Stakes

Offering collateral (vehicle, savings account, or other assets) typically results in lower interest rates and easier approval. However, defaulting means losing whatever was pledged as security.

Consider when: Credit challenges make unsecured loans prohibitively expensive, and the collateral asset isn't essential for daily life.

Unsecured Loans: Higher Rates, Lower Risk

No collateral requirements mean approval depends entirely on creditworthiness and income. While interest rates are typically higher, personal assets remain protected even if repayment becomes difficult.

Consider when: Preserving assets is more important than minimizing interest costs, or when collateral isn't available.

Making Smart Decisions

Compare multiple lenders since they serve different credit profiles. After approval, set up automatic payments and pay extra when possible to reduce total interest costs.

Before Applying

- Calculate the true cost: Use online calculators to determine total repayment amounts across different lenders.

- Explore alternatives: Could family, friends, employer advances, or credit union loans provide better terms?

- Assess repayment ability: Ensure monthly payments fit comfortably within the budget, accounting for other expenses.

During the Process

- Compare multiple offers: Different lenders serve different credit profiles—what one rejects, another might approve at reasonable terms.

- Read everything: Understanding terms prevents surprises and helps identify predatory lending practices.

- Ask questions: Legitimate lenders welcome questions about their products and processes.

After Approval

- Set up automatic payments: This prevents missed payments and potential fees.

- Pay extra when possible: Additional principal payments reduce total interest costs.

- Payoff plan: Consider how this debt fits into broader financial goals.

Direct deposit loans can provide valuable emergency funding when used responsibly. The key is understanding their proper role: short-term solutions for genuine emergencies, not long-term financial strategies or routine budget supplements.

Success with direct deposit loans comes down to three factors: borrowing only what's needed, choosing reputable lenders with reasonable terms, and having a clear repayment plan before signing anything.

When facing financial emergencies, these loans offer speed and accessibility that traditional lending often can't match. Just remember that convenience and speed typically come with higher costs, making careful comparison shopping and responsible borrowing practices more important than ever.

Related Frequently Asked Questions (FAQs)

Here are the questions people most often ask about direct deposit loans.

How Fast Can I Get Funds?

Some lenders offer same-day funding, but typically you’ll receive the money within one business day after approval.

Will Applying for a Direct Deposit Loan Hurt My Credit?

Simple Fast Loans performs a soft credit check during the application process, which does not affect your score.

Do I Need to Provide Collateral?

Not for unsecured loans. Secured loans, like title loans, require an asset as collateral.

What If I Can’t Repay on Time?

Missing payments can result in fees, credit damage, or even loss of collateral for secured loans. Always contact your lender early if issues arise.