Pending vs. Processing vs. Posted Payments, What Do They Mean?

Written by: Jacob S.

Published on:

Payment status labels—pending, processing, and posted—are frequently misunderstood, yet they play a critical role in financial management. These seemingly minor distinctions can trigger late fees, overdraft charges, and even negative marks on credit reports. Understanding the difference between when money appears to leave an account and when it actually completes its journey through the banking system can prevent costly mistakes and protect financial standing.

The confusion stems from how modern payment rails operate. Banks, payment processors, and financial institutions each handle transactions differently, with varying timelines and settlement rules. What consumers see in their account doesn't always reflect the technical status behind the scenes, creating a gap between perception and reality that can lead to missed due dates and unexpected fees.

Key Takeaways:

- Only posted payments count as officially received by creditors and lenders—pending and processing statuses don't satisfy due date requirements

- Initiating a payment on the due date is often too late, as most payments need 1-5 business days to fully post

- Late fees can be charged even when payments are "in progress" if they don't post by the due date

- Building a 3-5 business day buffer before due dates eliminates most timing-related payment problems

- Payment timing issues are especially critical for loans with fixed schedules and can affect credit reporting

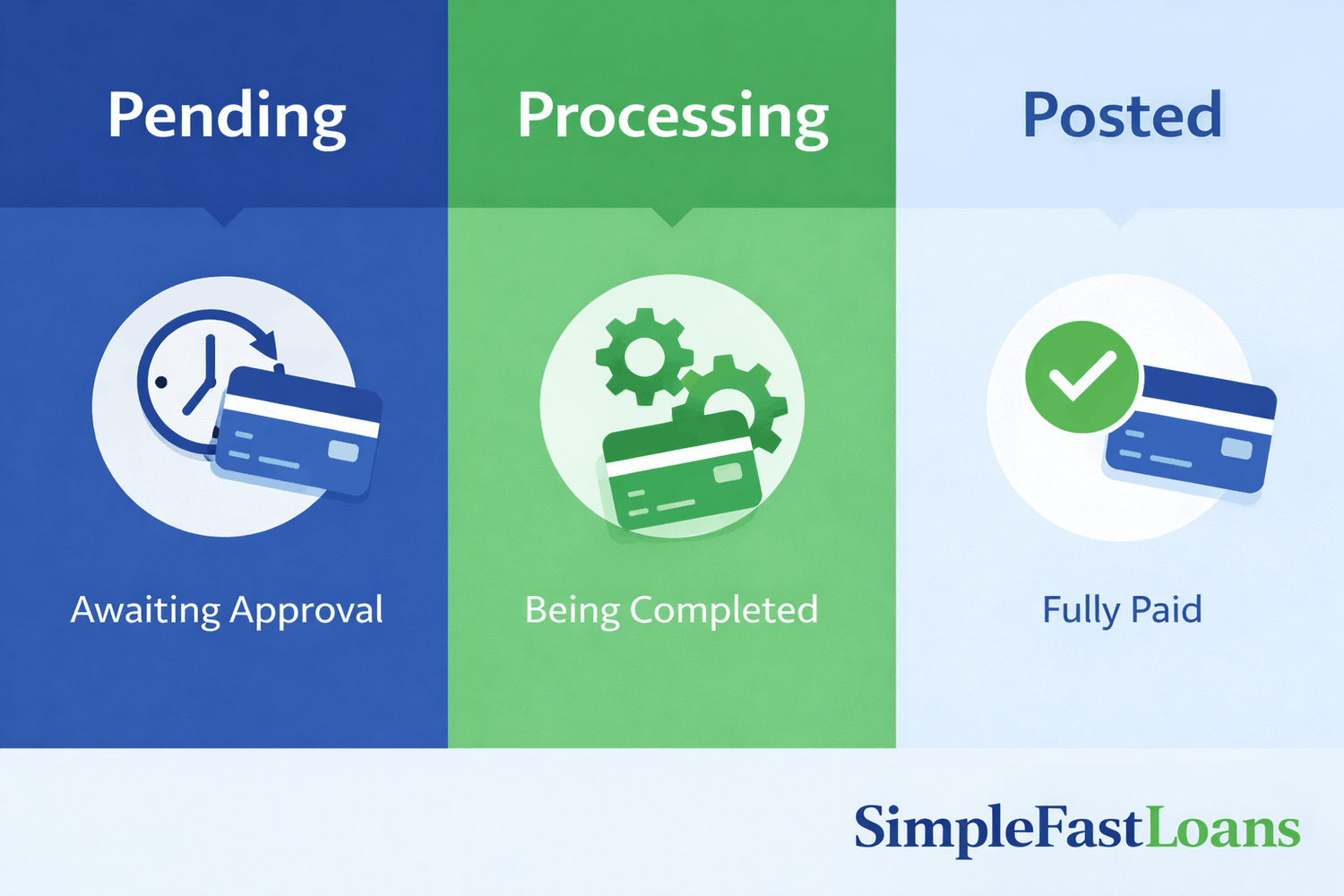

Understanding Payment Status: Pending, Processing, and Posted Defined

Payment status labels represent specific stages in the transaction lifecycle, each with distinct characteristics and implications for account balances and payment obligations. Understanding these definitions clarifies why timing matters and how financial institutions determine when payments are officially received.

- Pending refers to a transaction that has been authorized but not yet settled. The bank has verified funds are available and earmarked them for the transaction, but the money hasn't actually moved between accounts. Pending transactions reduce the available balance but don't affect the actual ledger balance until they post.

- Processing indicates a transaction is actively moving through the payment system. Authorization is complete, and settlement has begun, but the receiving institution hasn't yet credited the funds to the payee's account. Processing transactions is difficult to cancel and typically takes one to three business days to complete.

- Posted means the transaction has fully settled. Funds have been transferred, both institutions have updated their records, and the transaction is final. Only posted transactions count toward meeting payment due dates, satisfying loan obligations, and affecting credit reporting.

Why Payment Statuses Matter More Than Most People Realize

Financial institutions, lenders, and merchants treat each payment status differently, and these distinctions carry real consequences. A payment initiated by a consumer doesn't immediately translate to a payment received by a creditor. This lag exists across virtually all payment types, from rent checks to credit card payments to loan installments.

The timing gaps create predictable problems in specific scenarios:

- Rent and utility payments: Landlords and utility companies typically require funds to be fully posted by the due date. A payment showing as "pending" on the 1st of the month may not post until the 3rd, potentially triggering late fees even though the tenant initiated the payment on time.

- Loan and credit card due dates: Lenders almost universally base on-time payment determination on posted dates, not initiation dates. A loan payment submitted on the due date but still being processed the next day can be recorded as late, affecting both fees and credit reporting.

- Direct deposit delays: When direct deposits are pending and paychecks arrive later than expected, scheduled auto-payments may attempt to withdraw funds that haven't posted yet, resulting in overdrafts or returned payment fees despite sufficient incoming funds.

- Merchant refunds and returns: Product returns may show as pending for several days before the refund posts, creating a temporary shortfall if the original purchase amount was needed for other expenses.

- Check deposits: Deposited checks often have extended holds during pending status, sometimes up to seven business days for large amounts, preventing access to those funds even though they appear in the account.

The fundamental issue: "money sent" does not mean "money received" in the eyes of most creditors and financial obligations.

What Is a Pending Payment?

A pending payment represents an authorization or instruction that has been initiated but not yet settled. At this stage, the financial institution has received notice that funds should be transferred, but the actual movement of money between accounts hasn't been completed.

The pending status involves a critical distinction: authorization versus settlement. Authorization means the bank has verified that funds are available and has earmarked them for the transaction. Settlement is the actual transfer process where funds move from one institution to another. A transaction can remain authorized for days before settlement begins.

| Stage | What Happens | Funds Status |

|---|---|---|

| Authorization | Bank verifies funds are available | Earmarked but not transferred |

| Settlement | Actual transfer between institutions | In transit |

| Posting | Transaction completes and records update | Fully transferred and recorded |

Typical pending timeframes range from 1-5 business days, depending on the payment method and the institutions involved. Debit card transactions at point-of-sale terminals often clear within 24 hours, while ACH transfers routinely take two to three business days.

Common Examples of Pending Payments

Several transaction types commonly appear in pending status:

- Debit card purchases: When a debit card is swiped, the merchant's bank requests authorization from the cardholder's bank. The funds are held but not immediately transferred, creating a pending period that usually resolves within one to two business days.

- ACH transactions: Automated Clearing House payments, including direct deposits, bill payments, and transfers between banks, operate on a batch processing system. These transactions are submitted in groups and can remain pending for two to three business days under normal conditions.

- Scheduled bill payments: Many banks allow consumers to schedule future payments. These appear as pending from the scheduled date until the payment is actually processed and posted.

- Pending loan payments: Loan payments submitted through online portals or mobile apps typically show as pending until the lender's system processes the batch and updates the loan account balance.

- Hotel and rental car holds: These businesses often place authorization holds for estimated charges plus a buffer amount, which can remain pending for several days even after checkout or vehicle return.

How Pending Payments Affect Available Balance

Banks display two types of balances: the current balance and the available balance. Pending transactions reduce the available balance immediately but don't affect the actual balance until posting occurs. This creates a common scenario where an account shows sufficient funds in the actual balance but insufficient funds in the available balance.

| Balance Type | Definition | Includes Pending? | What It Shows |

|---|---|---|---|

| Actual Balance | Ledger balance with posted transactions only | No | Money is officially in the account |

| Available Balance | Amount available for immediate use | Yes | Money minus pending holds |

| Current Balance | Same as the actual balance in most systems | No | Posted transactions only |

Overdrafts can occur even when the actual balance appears positive because banks process new transactions against the available balance. If multiple pending transactions are waiting to post, and a new transaction comes through, the account may overdraft despite appearing to have adequate funds based on the ledger balance alone.

What Does "Processing" Mean?

Processing status indicates that funds are actively moving through the payment system. The authorization phase has completed, and the transaction has entered the settlement phase, where financial institutions exchange funds and update their records. At this point, the payment has left the control of the sender but hasn't yet been credited to the receiver's account.

Most payment types cannot be canceled once they reach processing status. The instructions have been submitted to the payment network, and the only way to reverse the transaction would be through a separate reversal request, which isn't always possible depending on the payment type.

Processing Timeframes by Payment Type

Different payment methods have distinct processing windows:

| Payment Type | Typical Processing Time | Business Days | Factors That Extend Timeline |

|---|---|---|---|

| ACH Standard | Overnight processing | 2-3 days | Weekends, holidays, cut-off times |

| ACH Same-Day | Expedited processing | Same day to 1 day | Higher fees, earlier deadlines |

| Debit Card | Faster verification | 1-2 days | Merchant settlement timing |

| Credit Card | Additional network steps | 3-5 days | Credit verification, merchant batching |

| Wire Transfer | Real-time processing | Same day | Bank hours, international transfers |

| Paper Check | Manual processing | 5-7 days | Mail time, bank policies |

ACH payments: The ACH network operates on a schedule with specific submission deadlines and processing windows. Standard ACH transfers typically process overnight, but the full cycle from initiation to posting takes two to three business days. Same-day ACH is available for certain transactions but comes with higher fees and earlier cutoff times.

Debit versus credit card payments: Debit card transactions usually process faster than credit card transactions because they involve immediate fund verification. Credit card payments must go through additional steps including merchant settlement and credit card network processing, which can extend the processing window to three to five business days.

Loan and installment payment processing windows: Lenders often batch process payments once or twice per day. A payment submitted at 11 a.m. might not begin processing until the afternoon batch runs, and then takes an additional 24 to 48 hours to fully post to the loan account.

Why Processing Payments Still Don't Count as Posted

Several factors prevent processing payments from being immediately recognized as complete:

- Bank cut-off times: Financial institutions establish daily cut-off times, typically in the afternoon. Transactions initiated after the cut-off time are processed the next business day, effectively adding 24 hours to the settlement timeline.

- Weekends and federal holidays: Payment networks and banks generally don't process transactions on weekends or federal holidays. A payment initiated on Friday afternoon may not begin processing until Monday, and might not post until Tuesday or Wednesday.

- Batch processing delays: Rather than processing each transaction individually, banks and payment networks use batch processing to handle thousands or millions of transactions simultaneously. These batches run on schedules, not continuously, creating waiting periods between submission and processing.

- Interbank settlement timing: Different banks have different settlement schedules with each other. A transaction between two major banks might settle faster than one between a small credit union and a large national bank.

What Is a Posted Payment?

Posted status means the transaction has fully settled. The funds have completed their journey from the payer's account to the payee's account, and all relevant balances have been updated. This is the point at which the transaction becomes final and irreversible through normal channels.

When a payment posts, several things happen simultaneously:

- The sender's account balance decreases by the payment amount

- The receiver's account balance increases by the same amount

- Both institutions' internal ledgers are updated to reflect the completed transaction

- The transaction moves from the pending or processing queue into the permanent transaction history

- The payment becomes eligible for recognition by credit bureaus and lenders for reporting purposes

Why Posted Status Is the Only Status That Counts for Due Dates

Lenders, creditors, and service providers universally define "on-time" payments based on posted dates, not initiation dates or processing dates. This policy exists because posted status is the only point at which the receiving institution has actually received and recorded the funds.

Credit reporting agencies follow the same standard. A payment must be posted by the due date to be reported as on-time. If a payment posts even one day after the due date, the lender may assess a late fee, though most don't report to credit bureaus until payments are 30 days past due.

Loan servicing agreements typically specify that payments must be "received" by the due date, and "received" is interpreted as posted. Screenshots showing a payment was initiated before the due date generally don't satisfy this requirement, as the lender's system only recognizes posted transactions.

Pending vs. Processing vs. Posted: A Side-by-Side Comparison

| Characteristic | Pending | Processing | Posted |

|---|---|---|---|

| Status Definition | Authorization received; funds earmarked but not transferred | Funds actively moving between institutions | Transaction complete; balances updated |

| Can Funds Be Reversed? | Yes, relatively easy to cancel | Difficult; requires reversal request | No, only through the dispute process |

| Counts as Paid for Loans? | No | No | Yes |

| Affects Credit Reporting? | No | No | Yes, if posted by due date |

| Typical Duration | 1-5 business days | 1-3 business days | Permanent |

| Shows in Available Balance? | Yes, reduces available funds | Yes, reduces available funds | Yes, reflected in all balances |

| Can Be Canceled? | Usually yes | Rarely | No |

| Visible to Payee? | Sometimes, depends on the system | Usually yes | Always |

Can a Payment Be Late If It's Pending or Processing?

Yes, the single most common cause of unexpected late fees is the misunderstanding that initiating a payment on the due date means the payment is on-time. Virtually all lenders and creditors require payments to be posted, not just initiated, by the due date.

Lender payment policies are explicit on this point, though the details are often buried in loan agreements or terms of service. The standard language states that payments must be "received" by a specific date, and received is defined as posted to the account. Some lenders offer a grace period of several days after the due date, but this grace period applies to the posted date, not the initiation date.

The distinction between posted date and initiated date creates a trap for consumers who reasonably believe that submitting a payment on the due date fulfills their obligation. From a technical standpoint, they've initiated the payment on time. From a contractual standpoint, they may still be charged a late fee if the payment doesn't post until after the due date.

Screenshots and confirmation numbers provide proof that a payment was initiated, but they don't protect consumers from late fees if the payment posts late. Some lenders will waive fees as a courtesy if shown evidence of timely initiation, but this is discretionary, not required.

How This Affects Different Payment Types

| Payment Type | Typical Late Fee | Grace Period | Credit Reporting Threshold | Key Risk |

|---|---|---|---|---|

| Personal Loans | $15-$50 or 5% of payment | 10-15 days | 30 days past due | Fixed due dates, no flexibility |

| Installment Loans | $25-$40 | 5-10 days | 30 days past due | Short payment cycles |

| Credit Cards | $30-$40 | 0-1 day | 30 days past due | High fees for repeat offenses |

| Mortgages | $50-100 or 4-5% of payment | 15 days | 30 days past due | Large fee amounts |

| Auto Loans | $25-$50 | 10 days | 30 days past due | Risk of repossession |

| Utilities | $5-$25 | 5-10 days | Not reported | Service disconnection risk |

Personal loans: Personal loan agreements typically specify exact due dates with no ambiguity about timing. Missing the due date, even by one day in posted status, can trigger late fees ranging from $15 to $50 or a percentage of the payment amount. Repeated late payments can also trigger default clauses in some agreements.

Installment loans: Installment loans, particularly those with weekly or bi-weekly payment schedules, are especially sensitive to timing issues because the payment windows are shorter. A payment that's two days late in posting might represent 10-15% of the payment period, compared to 6-7% for monthly payments.

Credit cards: Credit card issuers almost universally base on-time payment determination on posted dates. The Consumer Financial Protection Bureau has issued guidance that payments must be credited to accounts on the day they're received by a certain time, typically 5 p.m., but this applies to the date the payment posts, not when it's initiated.

Utilities and rent payments: Utility companies and landlords may have less sophisticated payment tracking systems, but they still typically base late fees on received or deposited dates. A check mailed and postmarked before the due date might not be considered on-time if it's not deposited and cleared by the due date.

How Pending Direct Deposits Can Cause Missed Payments

Direct deposits follow the same ACH processing rules as other electronic payments, meaning they can remain in pending status for one to three business days after the employer submits them. The timing depends on when the employer's payroll processor submits the batch, when the receiving bank processes incoming ACH transactions, and whether any weekends or holidays fall within the processing window.

Common reasons for direct deposit delays:

- Employer submits payroll file late or after ACH deadline

- Bank processing schedule doesn't align with employer submission timing

- Federal holidays interrupt the standard ACH processing cycle

- New employer or account requires additional verification steps

- Bank-specific hold policies for first-time or large deposits

Employers typically submit payroll files one to two business days before the intended pay date, which is why direct deposits often appear in pending status before the official payday. However, the actual posting time varies by bank. Some banks make direct deposits available as soon as they receive the ACH notice, while others wait until the official settlement date.

Banks have different policies about when to make pending direct deposits available. Some release funds early as a customer service feature, while others strictly adhere to the scheduled posting date. This variability means the same payroll submission can become available at different times depending on which bank receives it.

What Happens When Bills Are Due Before Funds Post

When auto-pay transactions are scheduled to coincide with payday, but the direct deposit posts later than expected, several problems can occur:

- Auto-pay failures: If an auto-pay transaction attempts to withdraw funds before a direct deposit posts, the transaction may be declined for insufficient funds. Even if the direct deposit is showing as pending and appears in the account balance, it may not be available for withdrawal, causing the auto-pay to fail.

- Late fees: Failed auto-pay attempts don't prevent the due date from passing. If the payment doesn't go through because funds weren't available, the creditor will typically assess a late fee even though the consumer had a pending direct deposit that would have covered the payment.

- Returned payment penalties: Some creditors charge separate returned payment fees in addition to late fees. A single failed auto-pay attempt can therefore result in multiple fees: a late fee from the creditor, an NSF fee from the bank, and a returned payment fee from the creditor.

- Service interruptions: Utilities, phone services, and subscription services may suspend access when auto-pay fails, requiring additional time and effort to restore service even after the payment eventually goes through.

Late Fees, Returned Payments, and Credit Impact

The financial cost of payment timing misunderstandings can accumulate quickly:

| Fee Type | Typical Amount | Who Charges It | Can Be Waived? |

|---|---|---|---|

| Late Payment Fee | $15-$50 | Creditor/Lender | Often, for the first occurrence |

| NSF Fee | $25-$35 | Bank | Rarely |

| Returned Payment Fee | $25-$40 | Creditor/Lender | Sometimes |

| Overdraft Fee | $30-$35 | Bank | Sometimes, with coverage |

| Re-attempt Fee | $25-$35 per attempt | Bank | Rarely |

| Utility Reconnection Fee | $25-$100 | Utility Company | Rarely |

- Late payment fees: Creditors typically charge $15 to $50 per late payment, with some calculating late fees as a percentage of the payment amount. Credit cards often charge $30 for the first late payment and $40 for subsequent late payments within six billing cycles.

- NSF fees: Non-sufficient funds fees are charged by banks when a transaction is attempted against an account without adequate available funds. These typically range from $25 to $35 per occurrence. Multiple transactions can trigger multiple NSF fees on the same day.

- Re-attempt charges: After a payment fails, some creditors automatically re-attempt the payment one or more times. Each re-attempt can generate additional NSF fees if funds still aren't available, potentially resulting in $75 to $105 in fees from a single missed payment.

When Late Payments Affect Credit Reports

Not all late payments immediately impact credit scores, but the risk exists whenever a payment posts after its due date:

- Grace periods: Most creditors don't report late payments to credit bureaus until they're 30 days past due. A payment that posts one week late may incur a late fee, but won't be reported to Experian, Equifax, or TransUnion. However, this grace period varies by creditor and isn't universal.

- 30-day reporting thresholds: Once a payment reaches 30 days past due, creditors typically report it to the credit bureaus. This reporting creates a negative mark that can remain on credit reports for seven years and significantly impact credit scores, especially for consumers with limited credit history.

- 60 and 90-day marks: Additional negative marks are added if payments reach 60 or 90 days past due, with each threshold causing further credit score damage. These extended delinquencies can make it difficult to qualify for new credit or favorable interest rates.

- Loan-specific policies: Different types of lenders have different reporting practices. Auto lenders and mortgage servicers are generally consistent about reporting 30-day late payments. Credit card issuers report monthly. Some personal and installment lenders may not report to credit bureaus at all, though they still charge late fees.

What to Do If a Payment Is Pending but a Due Date Is Today

When a payment is stuck in pending or processing status as a due date approaches, taking prompt action can minimize the consequences:

- Contacting the lender: Reaching out to the lender immediately, before the due date passes, creates a record of the situation and demonstrates good faith. Some lenders will note the account to waive late fees if the payment posts within a few days. Having a reference number from this conversation can be valuable if disputes arise later.

- Requesting fee waivers: Many lenders will waive a first late fee as a courtesy, especially if the account has a good payment history. Even if a late fee posts, it's worth calling to request a waiver. Success rates improve when consumers can document that the payment was initiated on time and the delay was due to processing times rather than insufficient funds.

- Providing payment confirmation: Having confirmation numbers, screenshots, or email receipts showing the payment was initiated before the due date doesn't guarantee fee waivers, but it improves the chances. Some lenders have policies allowing fee reversals when consumers can prove timely initiation.

- Making an additional expedited payment: In some cases, making a second payment via wire transfer or debit card (which posts faster) can satisfy the due date while the original payment processes. Check with the lender about applying the faster payment first and refunding the delayed payment.

Preventive Strategies Going Forward

Avoiding payment timing issues requires building buffer time into the payment schedule:

- Scheduling payments earlier: The safest approach is to schedule all payments to post at least three business days before the due date. This buffer accounts for processing delays, weekends, and holidays. For critical payments like mortgages or car loans, five business days is even safer.

- Buffer balances: Maintaining a cushion in checking accounts equal to one or two months of bills prevents situations where pending deposits cause available balance shortfalls. While this requires holding more cash in low-interest checking accounts, the cost of foregone interest is typically far less than overdraft and late fee charges.

- Aligning bill due dates with pay cycles: Many creditors allow consumers to choose their due dates or will adjust due dates upon request. Aligning due dates to fall several days after payday creates a natural buffer and reduces the risk of timing mismatches between deposits and withdrawals.

- Setting up balance alerts: Most banks offer text or email alerts when balances fall below a specified threshold. These alerts provide warning of potential insufficient funds situations before auto-pay attempts occur.

- Using credit cards for regular bills: Paying recurring bills with credit cards adds a layer of buffer time, since the credit card payment isn't due until the statement period ends. This strategy only works if credit card balances are paid in full each month to avoid interest charges.

Understanding payment status terminology protects both financial standing and hard-earned money. The distinction between pending, processing, and posted isn't just technical jargon—it determines whether payments arrive on time, whether fees are assessed, and whether credit scores remain intact. Taking the time to learn how payment timing works and building appropriate buffers into payment schedules prevents the vast majority of timing-related financial problems.

Related Frequently Asked Questions (FAQs)

Here are questions people often ask about pending, processed, and posted payments:

Does a pending payment mean the bill is paid?

No. A pending payment means the transaction has been initiated but not completed. Most creditors and lenders only recognize payments as received when they post to the account, not when they're pending. Relying on pending status to meet due dates will likely result in late fees.

Can a lender charge a late fee if payment is processing?

Yes. Lenders almost universally base on-time payment determination on posted date, not initiation date or processing status. If a payment is still processing on the due date and doesn't post until the next day, the lender can charge a late fee even though the payment was initiated on time.

How long can a payment stay pending?

Standard ACH payments typically remain pending for one to three business days. Debit card transactions usually clear within one to two days. However, weekends and holidays extend these timeframes. In some cases, particularly with checks or international payments, pending status can last five or more business days.

Do weekends and holidays delay posting?

Yes. Most payment networks and banks don't process transactions on weekends or federal holidays. A payment initiated on Friday afternoon typically won't begin processing until Monday and may not post until Tuesday or Wednesday. This can add three to four days to standard processing times.

What proof counts if a payment is disputed?

Confirmation numbers and screenshots showing payment initiation are useful but don't guarantee protection from late fees. They demonstrate good faith and improve the chances of fee waivers, but since most lender agreements specify that payments must be "received" (posted) by the due date, proof of initiation doesn't necessarily prove the contractual obligation was met. Requesting fee waivers with this documentation is often successful, but it's at the lender's discretion.

Why does my bank show two different balances?

Banks display an actual (or ledger) balance showing only posted transactions, and an available balance that accounts for pending transactions and holds. The available balance is what matters for determining if new transactions will clear or if overdrafts will occur.

Can I cancel a payment that's pending?

Usually, yes, if it hasn't moved to processing status. Contact the bank immediately. Once a payment reaches processing status, cancellation becomes much more difficult and may not be possible depending on the payment type.

Do all lenders report late payments to credit bureaus?

No. Not all lenders report to credit bureaus at all, though most major lenders do. Those that do report typically wait until payments are 30 days past due before reporting them as late. Check with specific lenders about their reporting practices.