The 5 Foundations of Personal Finance

Written by: Jacob S.

Published on:

Personal finance can feel overwhelming, but at its core, financial health rests on five foundational principles. Whether starting from zero or optimizing an existing plan, these five foundations provide a clear, actionable roadmap. Mastering them in sequence accelerates long-term stability and significantly reduces financial stress.

Key Takeaways

- An emergency fund of 3–6 months of expenses is the first and most critical pillar of personal finance — it protects every other financial goal from being derailed by unexpected costs.

- High-interest consumer debt, particularly credit card debt carrying APRs of 18–30%, should be eliminated before directing significant money toward investing.

- A consistent monthly budget — whether using the 50/30/20 rule, zero-based budgeting, or another framework — is the engine that makes all other pillars possible.

- Starting retirement contributions early is one of the highest-impact financial decisions available; time in the market consistently outweighs the amount invested when contributions begin late.

- Long-term wealth is built through diversified, low-cost, consistent investing — not timing the market or chasing returns.

Contents

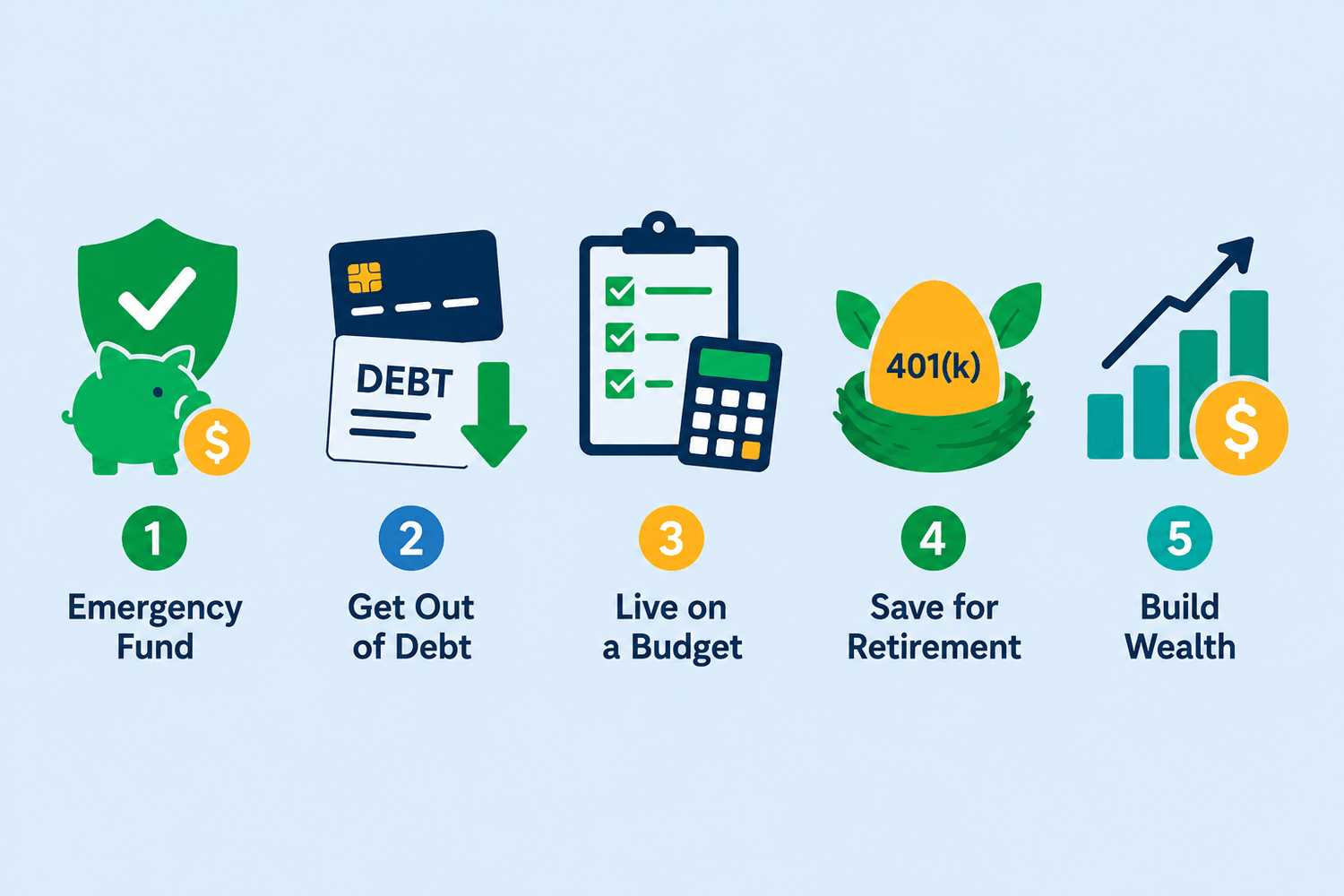

What Are the Five Pillars of Personal Finance?

The five pillars of personal finance are building an emergency fund, eliminating debt, living on a budget, saving and investing for retirement, and building long-term wealth. These five pillars provide a sequential framework for achieving financial stability — starting with protection against emergencies, progressing through debt freedom and intentional spending, and culminating in retirement security and generational wealth. Mastering each pillar in order gives individuals a clear, actionable path to lasting financial health regardless of income level.

Foundation 1: Build an Emergency Fund

An emergency fund is the bedrock of financial security. Without one, any unexpected expense — a medical bill, job loss, or car repair — forces reliance on high-interest debt, derailing other financial goals.

Rule of thumb: Aim to save 3–6 months of essential living expenses in a liquid, accessible account before aggressively pursuing other financial goals.

Why it matters

- Prevents debt accumulation during life disruptions

- Reduces financial anxiety and improves decision-making

- Creates a stable launchpad for investing and debt payoff

- Protects long-term investments from being liquidated prematurely

How much to save

The right target depends on household circumstances:

- Single income, stable employment — 3 months of expenses

- Dual income household — 3 months of expenses

- Single income, variable employment — 6 months of expenses

- Self-employed or freelancer — 6–12 months of expenses

- Household with dependents — 6 months of expenses

Where to keep an emergency fund

- High-yield savings account (HYSA) — easily accessible, earns interest above traditional savings rates

- Money market account — slightly higher yields with FDIC-insured protection

- Separate bank from checking — reduces temptation to spend the fund on non-emergencies

Related: How much cash should you keep on hand?

Foundation 2: Get Out of Debt

Debt — especially high-interest consumer debt — is one of the greatest barriers to wealth building. Every dollar paid in interest is a dollar that cannot compound in investments. Eliminating debt frees up cash flow and reduces financial risk.

As of 2024, the average U.S. credit card balance sits at $7,236, with average APRs exceeding 21% and total national credit card debt surpassing $1.14 trillion (Federal Reserve).

Two proven debt payoff strategies

Debt Avalanche — Pay minimums on all balances, then direct every extra dollar toward the highest-interest debt first. This method minimizes total interest paid and is mathematically optimal.

Debt Snowball — Pay minimums on all balances, then direct extra payments toward the smallest balance first. This method builds momentum through quick wins and works well for people who need motivation to stay on track.

Debt priority order

- High-interest consumer debt first — credit cards and payday loans typically carry 18–30% APR and should be eliminated as aggressively as possible

- Personal loans and auto loans — moderate interest rates with fixed payoff timelines

- Student loans — often carry lower rates; explore income-driven repayment options before overpaying

- Mortgage last — typically the lowest rate of any debt, and interest may be tax-deductible

Note on "good" vs. "bad" debt: Not all debt carries the same urgency. Low-interest mortgage debt (under 5%) may be less pressing to eliminate than high-interest credit card debt. Context matters.

Related: Is it better to save or pay off debt first?

Foundation 3: Live on a Budget

A budget is not a restriction — it is a spending plan. Without intentional allocation of income, money quietly disappears into non-essential categories, making saving and debt payoff far harder. Monthly budgeting creates awareness and control.

Popular budgeting frameworks

50/30/20 Rule — Allocate 50% of take-home pay to needs, 30% to wants, and 20% to savings and debt repayment. Best for beginners who want a simple, flexible starting point.

Zero-Based Budget — Every dollar is assigned a specific job so that income minus all allocations equals zero. Best for detail-oriented people who want complete visibility and control.

Pay Yourself First — Automatically save or invest a set percentage of income before spending anything else. Best for higher earners with variable discretionary habits.

Envelope Method — Cash or digital envelopes are created for each spending category, and spending stops when the envelope is empty. Best for overspenders who need firm category limits.

Key components of a functional budget

- Fixed expenses — rent or mortgage, insurance, and loan minimums that don't change month to month

- Variable necessities — groceries, utilities, and transportation that fluctuate but remain essential

- Discretionary spending — dining out, entertainment, and subscriptions; the most controllable category

- Savings and investments — treated as a non-negotiable expense, not an afterthought

- Irregular expenses — car registration, annual subscriptions, and gifts; divide these annually and set aside a monthly amount to avoid surprises

Budgeting tool options: YNAB, Monarch Money, spreadsheet templates, and bank-native tools all support different budgeting styles. The best tool is the one used consistently.

Foundation 4: Save and Invest for Retirement

Retirement savings are where wealth begins compounding at scale. The earlier contributions start, the more time compound interest has to work. Delaying by even a few years can result in significantly less wealth at retirement — a gap that is nearly impossible to fully close by saving more later.

A 25-year-old investing $300/month at a 7% average annual return reaches approximately $798,000 by age 65. A 35-year-old investing the same amount reaches roughly $379,000 — less than half, despite saving for only 10 fewer years.

Key retirement accounts (U.S., 2024)

401(k) — Traditional — Contributions are pre-tax, reducing taxable income today. Withdrawals in retirement are taxed as ordinary income. The 2024 limit is $23,000 ($30,500 if age 50+). Employer matching is common.

401(k) — Roth — Contributions are made after tax, but growth and qualified withdrawals are tax-free. Same contribution limits as Traditional. Employer matching is common.

Roth IRA — After-tax contributions with tax-free growth and withdrawal. 2024 limit is $7,000 ($8,000 if 50+). No employer match; income limits apply.

Traditional IRA — Contributions may be tax-deductible depending on income and employer plan access. 2024 limit is $7,000 ($8,000 if 50+). Taxed on withdrawal.

HSA (if eligible) — Available to those enrolled in a high-deductible health plan. Offers a triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. 2024 limits are $4,150 for individuals and $8,300 for families.

Recommended investment priority order

- Contribute to the employer 401(k) up to the full employer match — this is free money and should always be captured first

- Max out an HSA if enrolled in a high-deductible health plan

- Max out a Roth IRA if income-eligible, for tax-free retirement growth

- Return to the 401(k) and increase contributions toward the annual limit

- Open a taxable brokerage account for additional investing beyond tax-advantaged limits

Foundation 5: Build Wealth and Give Generously

The fifth foundation represents the long-term expression of financial success — building assets that generate passive income, protect against inflation, and eventually create freedom of time and choice. For many, this phase also includes intentional giving, recognizing that financial abundance enables meaningful contribution to causes and communities.

Core wealth-building vehicles

- Index funds and ETFs — the foundation of most long-term portfolios; low-cost, diversified, and historically averaging 7–10% annual returns

- Rental real estate — generates passive income and appreciation, though it requires capital, active management, and carries low liquidity

- REITs (Real Estate Investment Trusts) — provide real estate exposure without direct property ownership and trade like stocks

- Small business or side income — creates active income diversification with scalable upside

- Bonds and fixed income — lower return potential but provide stability and act as a ballast during equity market downturns

Principles of long-term wealth building

- Diversification — spread risk across asset classes, geographies, and sectors

- Consistency — regular contributions through market cycles (dollar-cost averaging) outperform attempts to time the market

- Low-cost investing — a 1% expense ratio difference can reduce a portfolio by hundreds of thousands of dollars over 30 years

- Tax efficiency — maximize tax-advantaged accounts and consider asset location strategies in taxable accounts

- Estate planning — wills, beneficiary designations, and life insurance protect accumulated wealth and ensure it transfers as intended

Charitable giving vehicles

- Donor-Advised Fund (DAF) — contribute assets, take an immediate tax deduction, and grant to charities over time

- Qualified Charitable Distributions (QCD) — for those age 70½ or older, give directly from an IRA tax-free

- Appreciated stock donations — avoid capital gains tax while supporting charitable causes at full market value

Related Frequently Asked Questions (FAQs) About the Five Pillars of Personal Finance

Here are other questions people often ask about personal finance pillars:

What are the five pillars of personal finance?

The five pillars of personal finance are building an emergency fund, getting out of debt, living on a budget, saving and investing for retirement, and building long-term wealth. Together, these pillars form a comprehensive framework for achieving and maintaining financial stability at any income level.

Do the five pillars of personal finance need to be followed in order?

Generally, yes — the sequence matters. Building an emergency fund before aggressively paying down debt prevents new debt from piling up during unexpected expenses. Eliminating high-interest debt before investing heavily ensures returns aren't wiped out by interest charges. That said, some steps overlap. Contributing enough to a 401(k) to capture an employer match, for example, is worth doing even while paying off debt.

How much money do I need before I start investing?

A fully funded emergency fund and zero high-interest consumer debt are the two prerequisites most financial experts recommend before directing significant money toward investing. The exception is always capturing the full employer 401(k) match first — that immediate 50–100% return on matched contributions is difficult to beat.

What is the most important of the five pillars of personal finance?

The emergency fund is widely considered the most foundational pillar because it protects every other goal. Without a cash cushion, any financial disruption — a job loss, medical bill, or major repair — forces reliance on debt, which unravels progress across all other pillars.

How long does it take to complete all five pillars of personal finance?

The timeline varies significantly based on income, debt load, and cost of living. Some people build an emergency fund in under a year and eliminate consumer debt in two to three years. Others manage all five pillars simultaneously over a decade or more. The goal is consistent forward progress, not speed.

Can someone work on multiple pillars at the same time?

Yes, to a degree. Contributing to a retirement account while paying off debt is a common and often smart approach, especially when an employer match is available. The key is avoiding spreading resources so thin that progress stalls on every front. Most financial planners recommend prioritizing one or two pillars at a time while maintaining minimums on others.

What if there isn't enough income to follow all five pillars of personal finance?

Start small. Even a $500–$1,000 starter emergency fund provides meaningful protection before shifting focus to debt. A budget built on a tight income often reveals more flexibility than expected. The five pillars of personal finance are designed to be scalable — the principles apply regardless of income level, even if the pace differs.

Is homeownership part of the five pillars of personal finance?

Homeownership is not a standalone pillar, but it intersects with several of them. A mortgage is addressed in the debt pillar, home equity contributes to wealth building in the fifth pillar, and housing costs are a core fixed expense in any budget. Whether renting or owning is the right choice depends on individual financial circumstances, not a universal rule.

Sources

- Federal Reserve — Report on the Economic Well-Being of U.S. Households (2023): federalreserve.govIRS — Retirement Topics: Contribution Limits (2024): irs.gov

- Federal Reserve — Consumer Credit (G.19): Credit Card Debt Data: federalreserve.gov

- Vanguard — Dollar-Cost Averaging: Long-Term Strategy: investor.vanguard.com

- FDIC — Deposit Insurance Coverage: fdic.gov

- IRS — Publication 969: Health Savings Accounts (HSA): irs.gov